Utah’s real estate market presents compelling opportunities for rental property investors. The state’s growing population, strong job markets in tech and healthcare, and relatively stable housing dynamics create demand for quality rental properties. However, financing those properties requires navigating a landscape where traditional lenders and flexible specialists like LendSure Home Loans serve different investor needs. Understanding your financing options—and how they compare—helps you make informed decisions about which loan program aligns with your investment strategy.

Why Utah Investors Need Alternative Financing

Utah’s population and economic growth, particularly in tech and healthcare sectors, create strong rental demand. Utah’s real estate market trends reflect this opportunity, with market analysis showing Q3 2025 dynamics that reward investors positioning themselves strategically.

The state’s housing market research documents seasonal patterns and growth trends that favor those ready to move quickly on acquisitions. Yet many Utah property investors encounter the same challenge: traditional lenders evaluate borrowers based on personal income and tax documentation, not the income their properties generate.

Why Traditional Lenders Hold Investors Back

Consider a common scenario: You own a cash-flowing rental and want to buy another. A conventional lender requires proof of personal income—paystubs, W-2s, or tax returns—rather than fully recognizing rental income.

Lenders apply rental income multipliers that reduce usable cash flow, making it harder to qualify even when the property performs well. This is where DSCR loans change the equation. Instead of personal income, approval is based on what the property actually earns.

Understanding DSCR Loans: Qualification Based on Property Cash Flow

DSCR stands for Debt Service Coverage Ratio, measuring whether a property’s rental income covers its total monthly housing costs. LendSure uses this metric to underwrite investment properties. Monthly rental income is divided by total housing expenses—including principal, interest, taxes, insurance, and association fees (PITIA). A DSCR of 1.0 means income covers costs, while 1.25 reflects a 25% surplus.

LendSure finances properties with DSCRs as low as 0.75, with exceptions down to 0.25 when supported by strong equity or improvement plans. Unlike conventional loans, DSCR financing requires no tax returns, W-2s, or income verification—only bank statements, leases, and property details. Qualification is based solely on property performance.

Key DSCR Advantages for Utah Investors

DSCR loans remove personal income as a barrier, allowing W-2 employees, self-employed investors, retirees, and those with non-traditional income to qualify equally. Investors can finance multiple properties at once, as LendSure supports simultaneous closings without mandatory waiting periods.

For active portfolio builders, loan amounts reach up to $3 million for 1–4 unit properties, with competitive options for 5–10 units. Purchase LTVs up to 85% and cash-out refinances up to 75% provide meaningful capital for growth. This speed, flexibility, and access to capital make DSCR loans well-suited for scaling Utah rental portfolios.

Conventional Loans: When They Make Sense

Conventional financing can still work for some Utah investors—particularly when buying a primary residence you plan to rent later, or if you have strong, well-documented income and prefer traditional underwriting. These loans often offer lower interest rates and smaller reserve requirements, with typical DTI limits between 36% and 43%, though higher ratios may be allowed with compensating factors.

The tradeoff is documentation and flexibility. Conventional underwriting requires tax returns, employment verification, and detailed income analysis. Rental income is counted only partially—usually 75% of gross rent minus expenses—creating a gap between actual cash flow and qualifying income.

Limitations for Portfolio Builders

Conventional lenders also cap the number of financed properties, typically between 4 and 10, which restricts portfolio growth. Longer timelines—often 45–60 days due to documentation and appraisal requirements—can slow or derail acquisitions for Utah investors pursuing fast or simultaneous purchases.

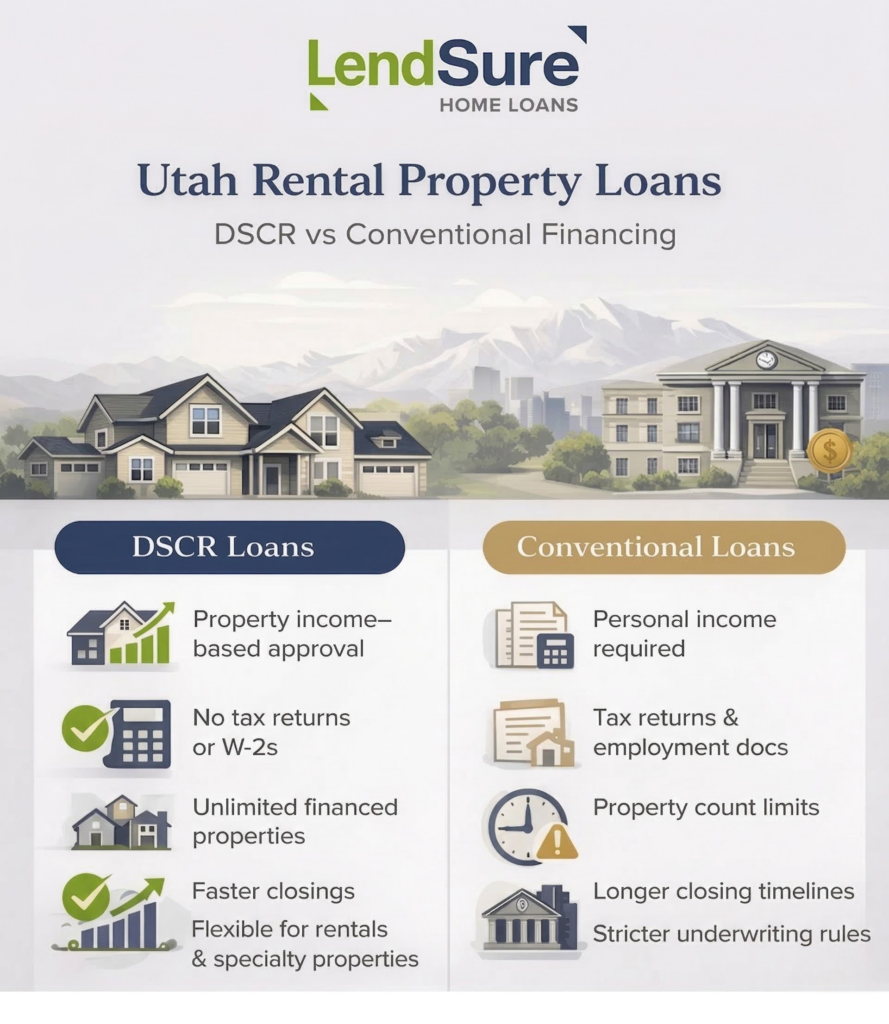

DSCR vs. Conventional: A Utah Investor Comparison

Income Documentation:

Conventional loans demand personal income proof—tax returns, paystubs, W-2s. DSCR loans require property income proof—bank statements, leases, property statements. For self-employed investors or those with complex income, DSCR eliminates documentation burden entirely.

Qualifying Income Calculation:

Conventional lending applies rental income multipliers and expense ratios that reduce the usable cash flow, sometimes by 25–50%. DSCR uses actual property income without personal income reduction, letting strong-performing properties qualify for larger loans and more aggressive expansion strategies.

Property Limits:

Conventional lenders cap financed properties, typically between 4 and 10. LendSure places no maximum on DSCR-financed properties, enabling unlimited portfolio expansion within the same investor’s borrowing capacity and competitive advantage.

Credit & FICO Flexibility:

Conventional loans typically require FICO scores of 620–740, depending on the program. DSCR loans accommodate FICO scores starting at 660, with flexibility for borrowers with recent credit events who demonstrate compensating factors like strong reserves or positive cash flow.

Closing Timeline:

Conventional loans require 45–60 days for underwriting, appraisal, and closing. DSCR loans deliver term sheets within 24–48 hours and close in 21–30 days, critical for investors competing in Utah’s active and competitive rental markets.

Cost Comparison:

DSCR loans carry slightly higher rates than conventional mortgages, reflecting the non-traditional underwriting model. However, the faster closing timeline and elimination of documentation burden often offset the rate premium for investors prioritizing speed and flexibility over marginal rate savings.

Special Considerations for Utah Rental Properties

Utah’s rental market includes property types that present challenges for conventional lenders. Utah’s rental market includes property types that conventional lenders often avoid.

Non-warrantable condos—such as buildings with high short-term rental use, commercial space, or concentrated ownership—face strict lending limits. LendSure finances these properties through DSCR programs, expanding access in condo-heavy markets like Salt Lake City and Park City.

Specialty Property Financing Options

LendSure also finances condotels, allowing investors to combine personal use with managed rental income, with purchase LTVs up to 75%. For investors pursuing renovations or ground-up construction, fix-and-flip financing is available for up to 90% of purchase price (experience-dependent) and up to 100% of construction costs.

Twelve-month interest-only terms help preserve cash flow during active project phases, supporting Utah investors in deals traditional lenders typically decline.

Why LendSure Serves Utah Investors Differently

LendSure’s approach is built around practical underwriting that reflects real investor scenarios. Loans are evaluated based on property performance—not personal income—creating clear advantages for Utah investors who need flexibility and speed. Streamlined underwriting enables fast approvals, with term sheets issued within hours and closings in as little as three weeks, helping investors move quickly in competitive markets.

Flexibility and Personalized Service

Flexibility is central to LendSure’s lending philosophy. Each deal is reviewed individually, allowing exceptions for lower DSCRs, higher leverage, or property types traditional lenders often reject. This people-first approach ensures personalized attention rather than rigid checkbox underwriting.

LendSure recognizes that investor goals and financial structures vary widely. Whether you’re a W-2 employee entering real estate, a self-employed investor scaling a portfolio, or a high-net-worth buyer with complex assets, LendSure matches you with financing tailored to your specific strategy.

Finding the Right Financing Path

Choosing between DSCR and conventional financing depends on your goals, timeline, and financial profile. Conventional loans may make sense for a primary residence you plan to rent later, offering lower rates and familiar underwriting. For investors building rental portfolios, pursuing multiple acquisitions, or financing properties traditional lenders avoid, DSCR loans offer the flexibility and speed that drive faster growth.

Utah’s rental market favors investors who act quickly. Market trends and seasonality show that rapid decision-making creates real advantages, as high-demand properties move fast. Financing that supports quick approvals and simultaneous acquisitions becomes a key competitive edge.

Strategic Portfolio Evaluation

Begin by reviewing your current portfolio and acquisition plans. How many properties do you expect to finance in the next 24 months? Does your personal income support conventional underwriting, or would property-based qualification be more effective? Are you targeting standard rentals, non-warrantable condos, or specialty properties that require flexible underwriting?

Your answers help determine whether DSCR loans through LendSure, conventional financing, or a strategic mix of both best supports your portfolio as it grows and evolves.

Ready to explore DSCR financing for your Utah rental properties?

Understanding your financing options is the first step toward building a successful Utah rental portfolio. Whether you’re considering DSCR loans, conventional financing, or a strategic mix of both, the right approach depends on your goals, timeline, and the opportunities in front of you.

LendSure Home Loans helps Utah investors navigate these decisions with personalized guidance based on their financial structure and property plans. Contact LendSure Home Loans to determine which loan program best aligns with your investment strategy and upcoming acquisitions.

LendSure Home Loans | Loans Made by People, for People Phone: 877.395.9002 | Email: info@lendsurehomeloans.com | Address: 12230 World Trade Drive, Suite 250, San Diego, CA 92128

NMLS ID# 1326437 (www.nmlsconsumeraccess.org)

Frequently Asked Questions

Can I use DSCR loans for both purchases and refinances in Utah?

Yes. LendSure funds DSCR purchases with LTV up to 85% for 1–4 unit properties, rate-and-term refinances up to 80% LTV, and cash-out refinances up to 75% LTV. This flexibility allows portfolio management alongside new acquisitions.

What happens if my property doesn’t have a lease when I’m purchasing?

LendSure can use market rent estimates based on comparable properties in your Utah area, supported by appraisal data. This enables purchase financing even when properties require tenant placement, critical for fix-and-flip conversions to rentals.

Do I need strong credit to qualify for DSCR financing?

LendSure works with FICO scores starting at 660, accommodating borrowers with credit challenges who demonstrate compensating factors—strong reserves, significant equity, or positive cash flow on existing properties.

How quickly can LendSure close a DSCR loan?

Term sheets typically arrive within 24–48 hours. Closings complete in 21–30 days on average, enabling rapid acquisitions in competitive Utah markets.

Can I finance multiple properties simultaneously with LendSure?

Yes. LendSure closes multiple loans for the same investor in a single transaction, with no maximum on total financed properties. This capability accelerates portfolio growth significantly.

What if I own a non-warrantable condo or condotel—can LendSure help?

Absolutely. LendSure finances non-warrantable condos and condotels that conventional lenders decline, up to 75% LTV for purchases. These specialty properties represent accessible opportunities in Utah’s diverse real estate market.

Is a DSCR loan right for every investor?

DSCR loans excel for portfolio investors, self-employed borrowers, foreign nationals, and those financing multiple properties. If you’re financing a primary residence or have straightforward W-2 income, conventional financing might serve you better. LendSure’s team can evaluate your specific situation and recommend the best option.