Financing a rental property in 2026 looks different depending on who you are, what you own, and how your income appears on paper. Conventional mortgages follow a well-documented path — tax returns, W-2s, and a debt-to-income ratio that neatly summarizes your financial life. But for many real estate buyers today, that path leads to a dead end.

Self-employed buyers, portfolio builders, and investors whose income lives inside a business rather than a pay stub often find that the most creditworthy version of themselves doesn’t fit the conventional mold. Knowing what qualifies you matters as much as knowing what you’re buying. LendSure Home Loans specializes in flexible financing for exactly this kind of borrower — with programs designed to work with your actual financial picture.

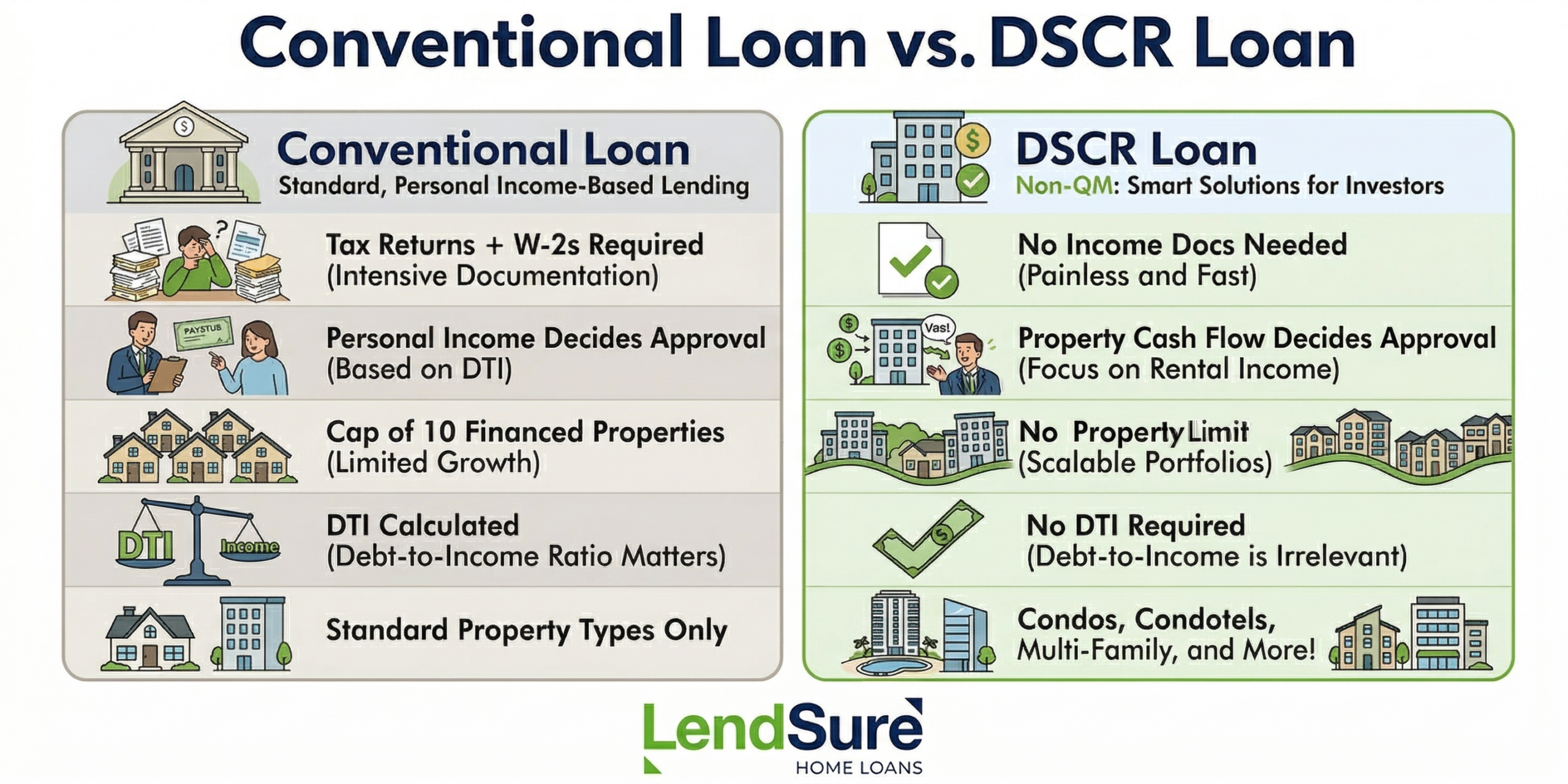

How Conventional Loans Approach Investment Properties

Conventional investment property loans follow agency guidelines set by Fannie Mae and Freddie Mac, which means full documentation: tax returns, W-2s, employment verification, and a debt-to-income ratio typically held to 36–43%. That documentation-heavy process reflects how these loans are underwritten — based on the borrower’s personal financial profile rather than the property’s income potential.

According to the FHFA, the 2026 baseline conforming loan limit for one-unit properties is $832,750, with high-cost area limits reaching $1,249,125 — meaning loans above those thresholds move into jumbo territory with their own stricter standards. Fannie Mae’s guidelines also cap conventional financing at 10 financed residential properties per borrower, a limit that stops many growing portfolios in their tracks.

How Conventional Lenders Count Rental Income

Rental income can factor into conventional qualification, but not always at full value. Fannie Mae’s rental income guidelines allow lenders to include documented rental income when calculating a borrower’s qualifying income — typically using lease agreements or Schedule E from tax returns. For buyers whose rental income is strong but whose personal income is modest on paper, this partial credit can still fall short of what’s needed to qualify.

What Is a DSCR Loan — and How Does It Change the Equation?

A DSCR loan — short for Debt Service Coverage Ratio loan — qualifies a buyer based on whether the property’s rental income can cover its full monthly housing costs, rather than on the borrower’s personal income. Lenders calculate DSCR by dividing the property’s monthly rental income by its total PITIA: principal, interest, taxes, insurance, and any association fees.

This structure is particularly well-suited for buyers whose tax returns understate their actual financial strength — a common situation for real estate investors who claim depreciation and business deductions. According to S&P Global Ratings, DSCR loans represented nearly half of collateral by balance in non-QM securitizations rated between July 2022 and July 2024, reflecting just how central this product has become to investment property financing. There are no W-2s, no pay stubs, and no DTI calculation involved — the asset does the qualifying.

Understanding the DSCR Ratio

A ratio of 1.0 means rental income exactly covers the full monthly housing obligation — break-even cash flow. Ratios above 1.0 signal additional cushion; ratios below signal that the property’s income doesn’t fully cover its costs, which typically requires compensating factors like stronger reserves or a larger equity position.

LendSure considers DSCR ratios as low as 0.75x, with exceptions available down to 0.25x for well-structured files. Most conventional rental income guidelines don’t offer this kind of flexibility — the property either qualifies or it doesn’t.

LendSure’s DSCR Program: Key Flexibility Points

LendSure’s Investor Cash Flow (DSCR) loan program is built around a common-sense underwriting philosophy that acknowledges real-world investment scenarios. Loan amounts reach up to $3 million for 1–10 unit properties, with purchase LTV up to 85% on 1–4 unit properties, rate-and-term refinances up to 80% LTV, and cash-out refinances up to 75% LTV.

Multiple loans for the same investor can close simultaneously, with no cap on properties owned or financed. Non-warrantable condos and condotels are also eligible. Buyers ready to run the numbers can price a DSCR loan directly through LendSure to see what their deal looks like.

Beyond DSCR: Other Loan Programs for Investment Property Buyers

DSCR financing is built for rental properties, but it isn’t the only option. Buyers with complex income structures may find other LendSure programs better suited to their situation.

Bank Statement Loans

Bank Statement Loans allow self-employed buyers to qualify using 12 or 24 months of personal or business bank statements instead of tax returns. Loan amounts reach up to $2 million, with LTV up to 85% and expense ratios as low as 10%. W-2 income can also be combined with bank statement income for a more complete financial pictureI.

Foreign National Loans

Foreign National Loans allow international buyers to purchase U.S. investment property without a Social Security number, U.S. tax returns, or domestic credit history. Borrowers can qualify using bank statements, CPA letters, employer letters, or property cash flow, with loan amounts up to $2 million and purchase LTV up to 75%.

Credit, Reserves, and What Lenders Are Actually Looking At

Even in programs that don’t rely on personal income, lenders evaluate creditworthiness through consistent lenses. Credit score is a factor in all LendSure programs, with qualifying scores generally starting at 660 — balanced against compensating factors like reserves and DSCR ratio. Fannie Mae’s eligibility matrix illustrates how conventional programs approach the same factors, often requiring stronger credit profiles and carrying significant pricing adjustments for lower scores.

Cash reserves are another underwriting consideration that buyers sometimes underestimate. Lenders want to see that a buyer can absorb a period of vacancy or an unexpected repair without defaulting. In DSCR programs, reserve requirements are expressed in months of PITIA, with requirements varying based on DSCR ratio and loan structure. Buyers who approach the process with strong liquid reserves often have more flexibility on other qualifying factors.

Property Eligibility: What Types of Investment Properties Qualify

Not all investment properties fit the same financing box, and that’s a key reason many buyers end up needing a non-conventional approach. LendSure’s DSCR program covers 1–10 unit residential properties, including property types that traditional lenders commonly decline.

1–4 Unit Properties

Single-family rentals, duplexes, triplexes, and fourplexes are the core of LendSure’s DSCR program. Loan amounts reach up to $3 million, with purchase LTV up to 85%, rate-and-term refinances up to 80% LTV, and cash-out refinances up to 75% LTV. These properties qualify based on rental income relative to PITIA, with no personal income verification required.

5–10 Unit Properties

Small multifamily properties with 5 to 10 units are also eligible under LendSure’s DSCR program, with loan amounts up to $2 million. This is a notable distinction from conventional financing, where properties above four units fall outside standard residential guidelines entirely and typically require commercial underwriting.

LendSure keeps these in the DSCR framework, qualifying them on property cash flow rather than pushing borrowers into a commercial loan process with different documentation, timelines, and terms.

Non-Warrantable Condos and Condotels

Non-warrantable condos — those that fall outside Fannie Mae’s eligibility criteria due to investor concentration, pending litigation, or other factors — are eligible under LendSure’s DSCR program. Condotels, which are hybrid properties combining individual ownership with hotel-style operations and optional rental management, are also eligible for both DSCR and dedicated condotel financing up to $3 million, with purchase LTV up to 75%.

Short-Term Rentals and Rural Properties

Short-term rentals with documented income from platforms like Airbnb or VRBO may also be used in DSCR calculations, subject to documentation requirements. Rural properties are considered as well, adding further flexibility for buyers in markets that larger lenders often overlook.

Working with a Lender That Looks at the Whole Picture

The difference between being approved and being declined often comes down to whether a lender is willing to look beyond the standard checklist. Conventional programs follow agency guidelines with limited room for interpretation. Non-QM programs like those offered by LendSure Home Loans are underwritten by people who understand that creditworthy buyers don’t always look the same on paper.

LendSure’s common-sense lending philosophy means that guidelines are a starting point, not a ceiling. Exceptions are considered when compensating factors support them: strong reserves, a lower DSCR with a large equity position, or a documented track record. Borrowers who want to explore where they stand can review LendSure’s full range of investment property loan options and connect with the team from there.

Frequently Asked Questions

Can I close a DSCR loan in an LLC?

Yes. LendSure’s DSCR program allows investors to close in the name of an LLC or other business entity, which many buyers prefer for liability protection and portfolio organization. This is one area where DSCR financing offers flexibility that conventional programs typically do not.

What cash reserves do lenders require for an investment property loan?

Reserve requirements vary by program and loan structure, but lenders generally want to see several months of PITIA held in liquid accounts after closing — enough to cover vacancies or unexpected expenses without defaulting. In DSCR programs, stronger reserves can also serve as a compensating factor when other qualifying elements are thinner.

What happens if a property has no existing lease at the time of purchase?

For properties without an active lease, lenders typically rely on a market rent appraisal to estimate income and calculate DSCR. LendSure’s program accommodates this scenario, meaning buyers don’t need a tenant already in place to qualify — the appraised market rent is used in underwriting instead.

How does rental income factor into a conventional mortgage application?

Under Fannie Mae’s rental income guidelines, lenders can include documented rental income — typically supported by lease agreements or Schedule E — when calculating a borrower’s qualifying income. However, this income is not always counted at full value, and buyers with modest personal income may still fall short of conventional qualification thresholds.

What documentation is needed for a short-term rental property?

For short-term rentals on platforms like Airbnb or VRBO, lenders typically look for documented rental history — platform statements, booking records, or a market rent appraisal. LendSure can use short-term rental income in DSCR calculations when properly documented, which opens the program to buyers pursuing vacation rental strategies.

Do DSCR loans work for condotels or non-warrantable condos?

Yes. LendSure’s DSCR program accepts both — property types that conventional lenders commonly decline. For condotel buyers specifically, LendSure also offers a dedicated condotel loan program with loan amounts up to $3 million and purchase LTV up to 75%.

Will LendSure make exceptions if my deal doesn’t fit standard guidelines?

LendSure reviews every scenario on a case-by-case basis. If a file has compensating strengths, such as higher reserves, a larger down payment, or a strong track record as an investor, those factors are weighed against areas where the deal falls outside standard parameters. This applies to borrower profile, property type, and deal structure. The best way to find out where you stand is to bring the deal to LendSure Home Loans directly and have it reviewed.