Colorado’s rental market continues to attract investors seeking opportunities in growing metros like Denver, Colorado Springs, and Fort Collins. Population migration, tech sector expansion, and strong employment growth fuel demand for quality rental properties.

However, securing financing for those properties requires understanding how traditional lenders and specialized programs like LendSure Home Loans evaluate borrowers differently. This guide helps Colorado investors navigate their financing choices and position themselves for success in a competitive market.

Colorado’s Rental Market: Context for Investor Decisions

Colorado’s real estate landscape has transformed significantly over the past decade. HUD’s Comprehensive Housing Market Analysis for Colorado documents rental market dynamics, vacancy trends, and demand patterns that shape financing decisions. The state’s housing data resources reveal consistent growth in rental demand, particularly in front-range communities where investor activity concentrates.

Understanding Colorado’s broader housing policy and market data helps investors place financing decisions in context. Strong job growth in Denver and steady military and tech demand in Colorado Springs support rental stability, yet many investors face obstacles with lenders who prioritize personal income over property performance. DSCR financing bridges this gap by focusing on what properties actually generate.

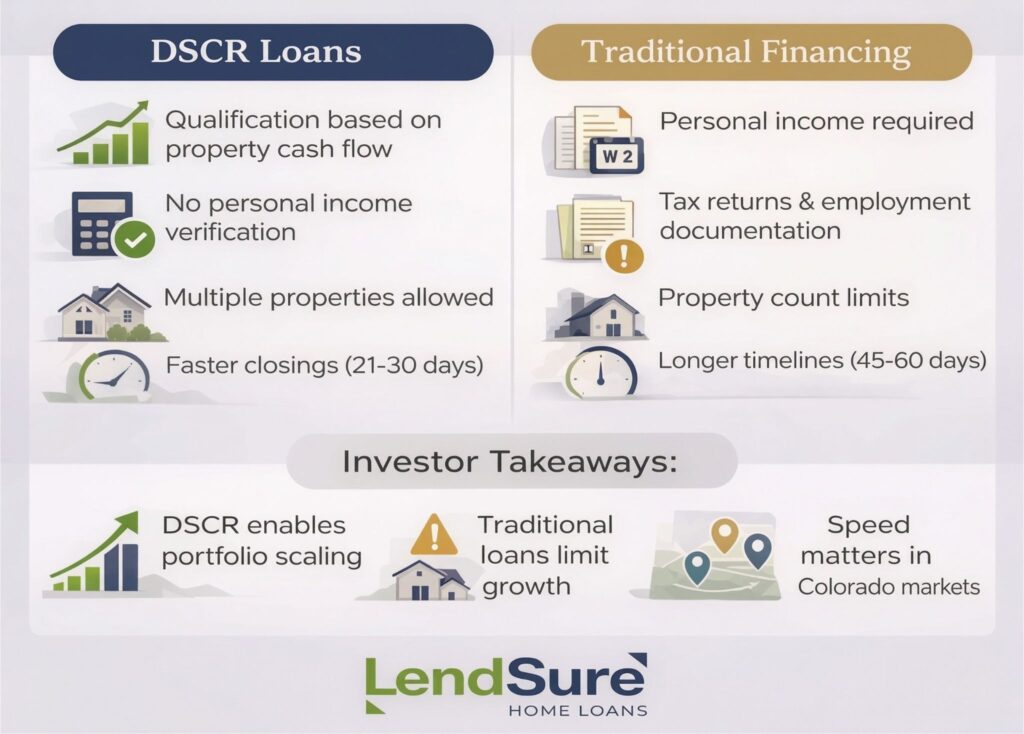

How Traditional Lenders Evaluate Colorado Rental Investors

Conventional financing for investment properties depends on personal income verification and heavy documentation, including tax returns, employment checks, and income analysis. For Colorado investors with stable W-2 income and strong credit, this approach can offer competitive rates and familiar loan structures.

For portfolio builders, however, conventional lending has limits. Lenders typically cap financed properties at 4–10 and apply rental income multipliers that discount 25–50% of actual cash flow. As a result, a Denver rental earning $2,800 per month may count far less toward qualification—especially for freelancers or business owners.

Documentation Burden and Timeline

Federal banking standards for commercial real estate lending establish underwriting norms requiring extensive clarifications and conditions. Between documentation requests, appraisal contingencies, and verification requirements, conventional closings typically span 45–60 days. For Colorado investors competing for properties in active markets, this timeline creates friction.

Understanding DSCR Loans: Property-Based Qualification

DSCR (Debt Service Coverage Ratio) financing fundamentally reverses the qualification equation. Instead of proving personal income through tax returns and paystubs, you qualify based on your property’s monthly rental income divided by its total housing costs (principal, interest, taxes, insurance, and association fees—PITIA). This metric directly measures whether a property’s cash flow supports the loan.

A DSCR of 1.0 means rental income exactly covers monthly obligations. A DSCR of 1.25 means the property generates 25% more income than required. LendSure finances Colorado properties with DSCR ratios as low as 0.75, with exceptions extending to 0.25—flexibility acknowledging real-world investor situations where strong equity or planned improvements justify lower initial ratios.

Key Advantages for Colorado Portfolio Builders

DSCR loans eliminate personal income as a limiting factor. Whether you’re a W-2 employee at a Colorado tech company, self-employed, retired, or support yourself through multiple income sources, your personal documentation doesn’t restrict your ability to finance investment properties. You provide bank statements, lease agreements, and property information. LendSure evaluates whether the property’s cash flow supports the loan.

You can finance multiple properties simultaneously. LendSure closes multiple loans for the same investor in a single transaction, enabling rapid portfolio expansion. Colorado investors benefit from this speed—no sequential waiting periods between acquisitions. Loan amounts reach up to $3 million for 1–4 unit properties, with purchase LTV ratios up to 85% and cash-out refinances up to 75% LTV.

Making the Colorado Financing Choice: Portfolio Impact Analysis

Your choice between DSCR and conventional financing sets the ceiling for portfolio growth. Conventional lenders impose hard limits—typically 4–10 financed properties—regardless of equity or performance. By contrast, LendSure DSCR programs place no cap on financed properties, allowing investors to scale as opportunities arise.

How the Programs Differ

- Conventional loans

- Personal income verification (tax returns, paystubs, employment letters)

- Rental income discounted 25–50% via multipliers

- Friction for self-employed investors whose tax returns understate earnings

- DSCR loans

- No personal income verification

- Qualification based solely on property cash flow

- Each property evaluated independently

Speed Advantage in Competitive Markets

- Conventional timelines: ~45–60 days

- DSCR timelines: term sheets in 24–48 hours, closings in 21–30 days

- Scaling benefit: DSCR allows multiple simultaneous closings; conventional lending is typically sequential, slowing growth

This combination of no property caps, property-based qualification, and faster execution gives DSCR financing a clear edge for Colorado investors pursuing rapid or multi-property expansion.

Colorado Property Types and Special Financing Needs

Colorado’s rental market includes property types challenging for conventional lenders. Non-warrantable condos—units in buildings with high short-term rental percentages, commercial space, or single-unit ownership—face conventional lending restrictions. LendSure finances these properties through DSCR programs, opening opportunities in Colorado’s condo-heavy markets like Denver and Boulder.

Condotel properties (hybrid ownership combining personal use with management-offered rental services) also qualify for LendSure financing. These specialty properties appeal to Colorado investors seeking dual-use opportunities in resort communities, and LendSure’s condotel programs accommodate up to 75% LTV for purchases.

Ground-Up Construction and Renovation Projects

Investors planning ground-up construction or significant renovation projects access LendSure’s fix-and-flip financing, available for up to 90% of purchase price (experience-dependent) and up to 100% of construction costs. Twelve-month interest-only terms preserve cash flow during construction phases—critical for Colorado investors managing active projects in competitive real estate markets.

Why LendSure Serves Colorado Investors Differently

LendSure focuses on practical underwriting built for real investor scenarios, financing based on property performance rather than personal income. This approach benefits Colorado’s diverse investor base and enables faster approvals, with streamlined processes that deliver term sheets within hours and closings in about three weeks.

Flexibility is central to LendSure’s philosophy. The company evaluates each deal individually, allowing exceptions for lower DSCRs, higher leverage, or property types traditional lenders decline. As a people-first lender, LendSure provides personalized attention that reflects each investor’s unique financial structure and goals.

Finding Your Financing Path in Colorado

Choosing between DSCR and conventional financing depends on your goals, timeline, and financial profile. Conventional loans may suit a single property you plan to rent later, while DSCR loans offer the speed and flexibility needed for portfolio growth, multiple acquisitions, or properties traditional lenders avoid.

Colorado’s rental market rewards investors who move quickly and adapt to opportunities. Research on housing market dynamics and investment patterns shows that strategic timing and rapid decision-making create competitive advantages. Properties in high-demand areas disappear fast. Financing enabling rapid decision-making and multiple concurrent acquisitions becomes a genuine competitive edge.

Strategic Portfolio Evaluation

Start by evaluating your current portfolio and acquisition plans. How many Colorado properties do you plan to finance in the next 24 months? Does your personal income comfortably support conventional lending, or do your financial situations benefit from property-based qualification? Are you targeting conventional apartment buildings, non-warrantable condos, or specialty properties requiring flexible underwriting?

These answers guide you toward DSCR loans through LendSure, conventional financing through traditional lenders, or strategically using both as your portfolio grows.

Your Colorado Financing Advantage

Colorado’s competitive rental market rewards investors who move quickly with flexible financing. DSCR loans remove personal income barriers, speed up closings, and support portfolio growth that conventional lenders often restrict. Whether you’re a W-2 employee, self-employed investor, or experienced operator scaling aggressively, your financing should support your strategy—not hold it back.

Take the Next Step

LendSure Home Loans helps Colorado investors evaluate their options with personalized guidance tailored to their goals and financial structure. Contact LendSure Home Loans to identify the financing path that positions you to move faster, qualify with confidence, and build a portfolio aligned with your vision.

LendSure Home Loans | Loans Made by People, for People

Phone: 877.395.9002 | Email: info@lendsurehomeloans.com

Address: 12230 World Trade Drive, Suite 250, San Diego, CA 92128

Frequently Asked Questions

Can I use DSCR loans for both purchases and refinances in Colorado?

Yes. LendSure funds DSCR purchases with LTV up to 85% for 1–4 unit properties, rate-and-term refinances up to 80% LTV, and cash-out refinances up to 75% LTV. This flexibility allows portfolio management alongside new acquisitions.

What happens if my Colorado property doesn’t have a lease when I’m purchasing?

LendSure can use market rent estimates based on comparable properties in your area, supported by appraisal data. This enables purchase financing even when properties require tenant placement, critical for fix-and-flip conversions to rentals.

Do I need strong credit to qualify for DSCR financing?

LendSure works with FICO scores starting at 660, accommodating borrowers with credit challenges who demonstrate compensating factors—strong reserves, significant equity, or positive cash flow on existing properties.

How quickly can LendSure close a DSCR loan?

Term sheets typically arrive within 24–48 hours. Closings complete in 21–30 days on average, enabling rapid acquisitions in competitive Colorado markets.

Can I finance multiple properties simultaneously with LendSure?

Yes. LendSure closes multiple loans for the same investor in a single transaction, with no maximum on total financed properties. This capability accelerates portfolio growth significantly.

What if I own a non-warrantable condo or condotel—can LendSure help?

Absolutely. LendSure finances non-warrantable condos and condotels that conventional lenders decline, up to 75% LTV for purchases. These specialty properties represent accessible opportunities in Colorado’s diverse real estate market.

Is a DSCR loan right for every Colorado investor?

DSCR loans excel for portfolio investors, self-employed borrowers, foreign nationals, and those financing multiple properties. If you’re financing a primary residence or have straightforward W-2 income, conventional financing might serve you better. LendSure’s team can evaluate your specific situation and recommend the best option.