Pennsylvania’s real estate market offers distinct opportunities for investors whose personal financial profiles don’t align neatly with traditional underwriting. DSCR loans—evaluated on property cash flow rather than borrower income—represent an increasingly popular financing path.

Lenders like LendSure Home Loans specialize in DSCR programs designed for real estate investors. This guide explains how DSCR lending works in Pennsylvania, what lenders actually require, and how it compares to conventional investment property financing.

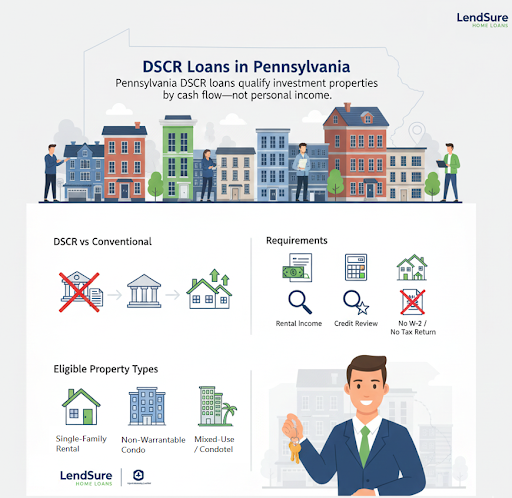

Understanding DSCR Fundamentals

DSCR stands for Debt Service Coverage Ratio, a measurement of how much rental income a property generates relative to its debt obligations. Divide the property’s annual net operating income by its total annual debt service (mortgage payment, insurance, taxes, HOA fees). A property generating $48,000 annually in net income with $40,000 in annual debt service carries a 1.2x DSCR.

Pennsylvania DSCR lenders assess properties based on cash flow rather than borrower income. This creates opportunities for entrepreneurs with complex business structures, physicians with business expenses, and landlords managing large portfolios. A Philadelphia entrepreneur running multiple ventures or a physician with documentation challenges may still qualify based on the property itself.

Pennsylvania’s Investment Landscape and Financing Implications

Pennsylvania offers diverse investment opportunities across urban, suburban, and rural markets. Pittsburgh’s revitalized neighborhoods, Philadelphia’s multi-unit conversion potential, and properties in Allentown, Erie, and Harrisburg attract investor interest for different reasons. This geographic diversity creates situations where traditional lenders and DSCR programs evaluate identical properties quite differently.

A multi-unit building in Pittsburgh’s Shadyside may fail under traditional guidelines if the borrower’s W-2 income can’t support the loan, even with strong cash flow. The same property could qualify through DSCR, where rental income supports the debt. Pennsylvania’s higher-tax counties also require stronger rents to meet DSCR ratios, a nuance lenders familiar with the state understand.

DSCR Loan Requirements

DSCR lending in Pennsylvania centers on property documentation rather than personal financial history. Lenders need lease agreements showing tenant commitments, property management statements documenting actual rent collection, recent bank deposits reflecting income received, and clear documentation of all property expenses including property taxes, insurance, utilities, and maintenance costs.

Credit, Down Payment, and Equity Expectations

Credit scores play a smaller role in DSCR lending, though lenders still review recent delinquencies or instability. LendSure accepts scores starting at 660, recognizing that credit events don’t always reflect investment performance. Down payments typically range from 15–25% for one- to four-unit properties, with higher equity sometimes required for multi-unit or more complex deals.

Loan Amounts and Property Categories

LendSure offers DSCR financing up to $3 million for one- to four-unit properties, covering everything from urban rowhouses to suburban and rural rentals. Five- to ten-unit properties typically cap at $2 million. Because DSCR focuses on stabilized cash flow, older or complex multi-unit properties—and renovation projects with clear income plans—can still qualify.

DSCR Ratios and Flexibility

DSCR ratios measure how well a property’s income covers its debt service. Traditional lenders usually require ratios of 1.25x or higher. LendSure accepts ratios as low as 0.75x for Pennsylvania properties, with exceptions down to 0.25x on a case-by-case basis. This flexibility supports investors acquiring underperforming or transitional assets, including renovation or lease-up projects.

Accounting for Seasonal Income Patterns

Properties in resort areas, college towns, or seasonal rental markets experience income fluctuations throughout the year. Instead of relying on single-month snapshots, lenders evaluate normalized income across multiple seasons to reflect long-term performance.

Documentation Speed and Underwriting

DSCR underwriting in Pennsylvania moves faster than traditional mortgage processes because evaluation centers on property documentation rather than personal financial review. LendSure typically provides term sheets within days, reducing uncertainty for active investors.

Documentation includes recent property management statements (current month plus at least two prior months), lease agreements or rental verifications, property tax bills, insurance declarations, and a detailed expense breakdown. For self-managed properties, bank statements showing rent deposits and expenses can substitute for management reports.

Loan Structure Options

Interest-only structures are common in DSCR lending, often featuring a 10-year interest-only period on a 40-year amortization. This structure minimizes monthly payments and preserves cash for improvements or additional acquisitions.

Amortization options typically range from 25 to 40 years depending on property type and lender preferences. Longer terms reduce monthly payments, while shorter terms accelerate equity building for investors with stronger cash flow.

Special Property Types and Non-Warrantable Condos

Pennsylvania’s condo market presents particular challenges for traditional lenders. Non-warrantable condos—properties in buildings without sufficient owner-occupancy or with rental restrictions—face systematic rejection from conventional lenders despite solid fundamentals. Philadelphia’s residential conversions and Pittsburgh’s downtown loft buildings sometimes fall into this category, limiting financing options to specialist lenders.

DSCR programs allow non-warrantable condos up to 75% LTV when cash flow supports the loan. This opens opportunities for investors purchasing condo conversions, urban properties, or assets in transitional neighborhoods. Condotels and mixed-use buildings with residential income also qualify, as lenders focus on property-specific cash flow rather than blanket restrictions.

Evaluating Your Financing Position

Understanding whether DSCR financing works for your Pennsylvania property requires examining your specific situation. Consider accessing 12 months of property management statements or personal banking records showing rental deposits to clarify how strongly your property supports debt service.

Assess Personal Debt and Income Constraints

Documenting your current personal debt obligations and income sources helps identify whether traditional lending constraints might affect financing approval.

Evaluate Credit History and Risk Factors

Review your credit history for recent delinquencies or judgments that provide context for lender evaluation.

Analyze Property-Specific Characteristics

Understanding your Pennsylvania property’s building age, unit configuration, neighborhood, vacancy rates, and renovation status indicates how traditional and DSCR programs may evaluate it differently.

Clarify Timeline and Expansion Goals

Clarifying your investment timeline and future expansion plans determines whether portfolio-building flexibility matters for your strategy.

These details form the foundation of conversations with lenders, helping narrow which program and lender match your circumstances most effectively.

LendSure’s Pennsylvania Investment Approach

LendSure brings localized lending understanding to Pennsylvania investment properties. Rather than applying national templates to regional markets, the team understands Pennsylvania’s tax structures and market dynamics. Philadelphia properties receive evaluation reflecting urban market realities. Pittsburgh investments get assessed within that region’s specific dynamics. Rural Pennsylvania properties receive consideration appropriate to their market characteristics.

This common-sense lending approach extends to flexibility on guidelines. An experienced Pennsylvania investor with detailed property management history might qualify with lower documentation requirements than a first-time investor. Complex financing situations receive individual evaluation rather than automatic rejection. This philosophy—loans made by people, for people—particularly suits Pennsylvania’s diverse investor base and varied property types.

Talk With LendSure About Your Investment Plans

If you’re considering a Pennsylvania investment and want financing aligned with your property’s real cash flow, contact LendSure to discuss your portfolio and acquisition goals. The team can help you evaluate DSCR options tailored to your market, timeline, and property type.

FAQs

What counts as net operating income for a Pennsylvania DSCR calculation?

Gross rental income minus actual property operating expenses. Include property taxes, insurance, HOA or condo fees, property management fees, maintenance costs, and utilities if the landlord pays them. Do not include capital improvements, debt service on other properties, or personal living expenses. LendSure works with borrowers to ensure accurate income documentation reflecting actual property performance.

Can I finance a Pennsylvania property purchase and renovation simultaneously with DSCR?

DSCR loans evaluate the stabilized property’s income production. If you’re renovating before stabilization, lenders typically base qualification on projected income once renovation completes. Renovation financing sometimes requires bridge loan structures or phased closings. LendSure can discuss whether acquisition and construction financing works as separate products or combined structure.

Does Pennsylvania’s property tax create challenges for DSCR qualification?

Pennsylvania’s property taxes rank among the nation’s highest in many counties, increasing required rental income for acceptable DSCR ratios compared to lower-tax states. However, experienced DSCR lenders understand Pennsylvania’s tax landscape and factor this into evaluation. Properties that seem undervalued compared to other states often reflect Pennsylvania’s tax burden already factored into pricing.

Can I use DSCR financing for a property I plan to eventually occupy personally?

DSCR loans structure around investment property income. If you’re considering owner-occupancy in the future, discuss this timeline with lenders early. Some programs accommodate plans for future primary residence occupancy; others don’t. LendSure can evaluate whether your timeline and intentions work within DSCR structure.

What happens if my property’s rental income drops after closing?

DSCR loans evaluate the property at origination based on documented income. Subsequent income changes don’t trigger immediate refinancing unless you’re seeking rate-and-term changes. However, if refinancing later, new income documentation would reflect current property performance. This is why accurate income documentation at origination matters—it represents the property’s demonstrated capability.

Are there financing restrictions on specific Pennsylvania neighborhoods or counties?

LendSure evaluates individual properties rather than restricting financing by geographic area. A well-performing property in any Pennsylvania neighborhood can potentially qualify if income supports debt service. Property-specific cash flow analysis determines eligibility regardless of location.

How does LendSure handle Pennsylvania properties with seller financing or owner-carry terms?

Seller-financed properties require clear documentation of financing terms, down payment, and interest rate. LendSure evaluates how the seller-financed debt impacts total property debt service when calculating DSCR. This sometimes creates challenges if seller financing carries unfavorable terms; lenders structure analysis around actual debt service obligations.